CommSec

CommSec

18 Mar 2025

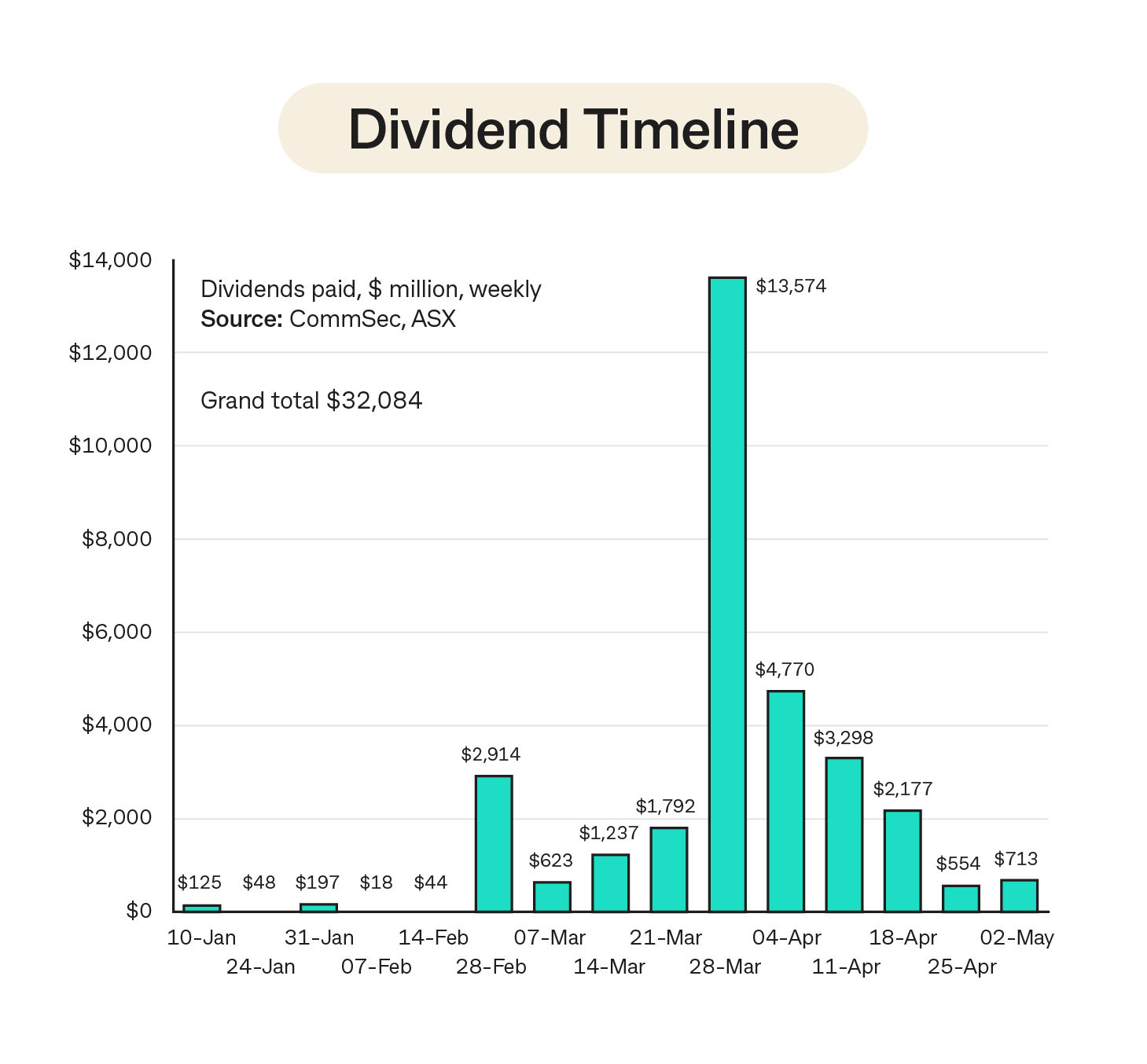

According to CommSec estimates, major Aussie companies classified in the S&P/ASX 200 index will pay out around $32.1 billion in dividends in the first five months of 2025, down 5.6 per cent from last year’s $34 billion.

While still significant, the amount of dividends declared by companies is the lowest for the February reporting season period since 2021, when capital-constrained businesses returned $25.8 billion to shareholders.

The S&P/ASX 200 index may have hit a record high last month, but the dividend “drought” continues with payouts dwindling after a resources-sector induced record $36 billion in dividends were declared in the February 2022 profit reporting season.

In the coming week, dividend payouts to investors start to ramp up. Dividends issued by S&P/ASX 200-listed companies will total a massive $13.6 billion in the week ending March 28 and then a further $11.5 billion over the following five weeks.

That said, lower dividend payments will hit bank accounts at a time of heightened market volatility, as investors worry about the impact of US President Donald Trump’s tariff threats on the global economy. On March 13, 2025, the benchmark S&P/ASX 200 index was down 10 per cent from its all-time high on February 14, 2025, which is commonly known as a market correction.

The crisis engulfing China’s property and construction sectors weighed on mining profits during Australia’s recent company reporting season, forcing commodity heavyweights, such as BHP, Rio Tinto and Fortescue to slash their dividends amid falling profits, declining capital returns and rising capital expenditure.

Mining shares represent a large proportion of the benchmark S&P/ASX 200 index – with an almost 19 per cent weighting for the materials sector – according to the latest data from S&P Global. While this weight has dipped from the recent peak of 25 per cent in late 2023, the cyclical nature of the sector means that a prolonged economic slowdown – as experienced in China and developed countries during the Covid-19 pandemic – will hit mining earnings, with fewer profits to pay the same level of dividends as before.

In the case of mining giant, BHP, the company paid a dividend of US62 cents per share in both March and September 2015, supported by the Chinese economic boom.

But its dividend slumped to just US16 cents and US14 cents per share, respectively, for the same period in 2016 as activity in the world’s second largest economy slowed. The payouts jumped to US$1.50-US$1.75 per share after commodity prices soared following Russia’s invasion of Ukraine in 2022.

BHP will pay shareholders about A$4 billion after declaring an interim dividend of just US50 cents per share in the latest reporting season, the lowest in eight years. The half-year dividend was 30% lower than the same time last year and the lowest since February 2017.

The dividend represented just 50 per cent of underlying earnings - the bare minimum promised to investors under BHP’s dividend policy as iron ore prices slipped. The dividend payout ratio was lowered to help BHP invest more in growth, particularly in commodities such as copper that are expected to enjoy increased future demand as the world electrifies.

BHP’s weaker dividend follows a broader trend in the resources sector, with Rio Tinto announcing its lowest dividend payment in seven years, citing higher production costs and weaker iron ore prices as key factors in an 8 per cent decline in full-year profit. Aussie shareholders will receive A$1.3 billion in payments, with a final dividend of $US2.25 per share on April 17, bringing total dividends for the year to $US4.02 per share – the lowest since 2017. That said, the payout remains within the company’s policy of distributing 40 per cent to 60 per cent of underlying earnings, with the latest dividend set at the upper end of that range.

Fortescue will pay shareholders about A$1.5 billion after slashing its dividend 54 per cent to 50 cents per share after reporting a significant decline in profit amid falling prices of the steel-making ingredient. That said, the dividend payout represented 65 per cent of the Financial Year 2025 first half’s net profit – the same as the Half Year 2024.

On the flipside, for the six months ended December 31, 2024, diversified miner South32 delivered an impressive turnaround in its performance with a significant jump in profitability compared to the prior corresponding period. Its profit after tax was up 577 per cent to US$359 million. South32's earnings per share rose from US1.2 cents to US8 cents. This allowed the company's board to increase its dividend by a whopping 750 per cent to US3.4 cents per share.

Oil and gas producers lower dividends

Oil and gas giant Woodside Energy was the third largest dividend payer in the February reporting season, announcing a payout of A$1.6 billion but was down 9.2 per cent on the previous period. It declared a final dividend of US53 cents per share, compared with US60 cents apiece last year, after reporting a 13 per cent drop in its full-year profit, hurt by lower realised prices which offset higher production.

Insurers hike dividends

Within the financials sector, it was a cracking reporting season for insurance company shareholders. Suncorp lifted its dividend 58 per cent, QBE Insurance 32.6 per cent and Insurance Australia Group 18.2 per cent.

QBE Insurance Group posted a 27% rise in its full-year profit, helped by growth in investment returns, premiums and lower catastrophe claims. The board raised the final dividend to 63 cents, with a total payout of $951.1 million to shareholders.

Suncorp shares hit record highs after it announced a capital return of $3 per share from net proceeds of the Suncorp Bank sale. The insurer declared a special dividend of 22 cents per share and an interim dividend of 41 cents apiece.

Insurance Australia Group posted a 54.2% rise in first-half cash earnings, benefiting from higher margins and lower natural perils costs. The general insurer announced an interim dividend of 12 cents per share, up from 10 cents a year ago, but lower than consensus estimate of 13.9 cents.

Elsewhere, the Commonwealth Bank (CBA) will pay shareholders A$3.8 billion after the lender’s first-half profit rose slightly as an improving economy enabled it to slash loan impairment charges. CBA also declared an interim dividend of $2.25 per share, up from $2.15 a year earlier, its highest first-half payout ever.

Blue chip companies lift dividends

In terms of other individual company dividends, Qantas Airways showered investors with its first post-pandemic ordinary dividend, and a special dividend, for the first time in a quarter of a century. The airline reported strong demand across its budget and full-service operations. Qantas reported 11 per cent year-on-year growth in underlying profit before tax for the six months that ended December 31, 2024 to $1.39 billion. It declared an interim dividend of 16.5 cents per share, the first payout since it paid 13 cents in September 2019. A special dividend of 9.9 cents was also announced for the first time since fiscal year 2000.

Telecommunications giant Telstra reported H1 25 profit of $1.03 billion, in-line with consensus estimates and ahead of last year's $964 million. Telstra also announced a $750 million on-market buyback. It declared a 9.5 cents per share interim dividend, up from 9 cents the prior year. Telstra’s payout to investors will total A$1.1 billion.

Australian biopharmaceutical company CSL said that falling immunisation rates in the US, its largest market, weighed on its vaccine sales and first-half profit growth. Overall net profit rose 6% to US$2.01 billion, driven by a 10% rise in revenue from CSL's main blood-plasma business Behring. CSL will pay a dividend of US$1.30 per share unfranked on April 9, 2025. The Financial Year 2025 dividend is 9 per cent higher than the Financial Year 2024 interim dividend. CSL will distribute just over A$1 billion to shareholders.

Supply chain logistics company Brambles posted upbeat half-year results, with underlying profit of $717.9 million, up 10% year-on-year on a constant foreign exchange basis for first half of Financial Year 2025. The Brambles board declared a 2025 interim dividend of US19 cents per share, up from US15 cents per share taking the total payout to A$418.3 million.

Power producer Origin Energy exceeded half-year earnings forecasts on Thursday with a 24% jump in underlying profit on strong liquefied natural gas sales, allowing the company to commit $1.7 billion to major battery projects. Origin’s underlying result, which beat the consensus estimate of $888.3 million, led it to declare an interim dividend of 30 cents, also above the market's estimate of 27 cents.

Australian share registry provider Computershare raised its annual earnings outlook and declared an interim dividend of 45 cents apiece, up 12.5 per cent from last year.

New Zealand-based but ASX-listed dairy producer The a2 Milk Company declared its first dividend and hiked its annual revenue growth outlook citing stronger-than-anticipated demand for its English-label infant milk formula. It declared an interim dividend of NZ8.5 cents per share and will continue to review capital management options, which could result in future capital returns to shareholders, likely in the form of special dividends.

Retail conglomerate Wesfarmers - owner of Kmart, Bunnings and Officeworks - declared an interim dividend of 95 cents per share, up from last year's 91 cents. Net profit was $1.47 billion for the six months to December, slightly ahead of consensus estimates of $1.45 billion and the previous year's $1.43 billion, helped by a 3.1 per cent increase in pre-tax profit at Bunnings, the company's main earner. Wesfarmers payout to investors will total A$1.1 billion.

JB Hi-Fi posted an 8% rise in its first-half profit, aided by strong sales across its operations. The company's net profit after tax for the half year ended December 31 rose to $285.4 million, up from $264.3 million a year earlier. The electronics retailer announced an interim dividend of 170 cents apiece, compared with 158 cents per share a year earlier.

Grocer Coles Group reported a first-half profit in-line with market expectations and declared its highest dividend in at least five years, helped by the holiday shopping frenzy and a strike at larger rival Woolworths. Underlying earnings at its Supermarkets segment, Coles' biggest money-making business, jumped more than 14% to $2.03 billion as consumers saddled with high living costs shopped for cheap and discounted items, particularly during the holiday season. Coles declared an interim dividend of 37 cents per share, its highest since fiscal year 2019, and slightly higher than 36 cents apiece distributed a year ago.

Top Australian supermarket chain Woolworths said first-half profit fell the most in a decade as rising living costs spurred bargain-hunting and a warehouse strike left shelves bare. It also warned the austerity would weigh on future results. Net profit excluding one-off items fell 20.6% to $739 million for the six months, missing the consensus estimate of $770 million. Woolworths cut its interim dividend to 39 cents per share from 47 cents last year.

Dividend outlook

While ASX-listed companies continue to generate strong income for investors, the economic backdrop remains challenging for Aussie firms operating in a higher inflation and interest rate environment. Trade and political uncertainty alongside slowing Chinese demand for commodities are weighing on company earnings.

S&P/ASX 200 index dividend payout ratios have been under pressure in recent years amid weaker earnings growth, with ASX-listed companies paying out less of those earnings as dividends to shareholders. The price of those earnings and dividends are also more expensive with the 12-month forward price-to-earnings (P/E) ratio for the ASX 200 index currently near 17x, trading above the historical long-term average around 15x.

That has resulted in a declining dividend yield for Aussie shares. In fact, the 12-month forward estimated dividend yield for the S&P/ASX 200 index at 3.7 per cent is currently trading about two standard deviations below the long-run average of 4.5 per cent since 2000. Put another way, the dividend yield has only been lower about 5 per cent of the time over the past 25 years.

A further challenge for investors will be generating dividend growth in the near-term. Benchmark heavyweights – the miners and banks – will likely encounter earnings growth pressures amid falling interest rates, intense lending competition and declining iron ore prices.

But it is not all bad news for income investors. Income specialist Plato Investment Management’s proprietary dividend cut model is currently showing that the probability of cuts is currently in the “normal range” going back to 2021. This implies that we may have seen the worst of dividend cuts at the index or market level for now.

The average dividend payout ratio on the S&P/ASX 200 index – the percentage of net income paid out to shareholders as dividends – has risen from near decade lows at 56 per cent in calendar year 2022 to 128.5 per cent in calendar year 2024, above the long-run average prior to the Covid-19 pandemic.

Even though the 12-month trailing dividend yield on the large cap S&P/ASX 200 index has now fallen to 3.7 per cent, thanks to a surge in the value of traditional “big four” banks, it still compares favourably with the 1.4 per cent on offer on the US benchmark S&P 500 index and the 2.7 per cent yield offered by the MSCI Asia-Pacific index.

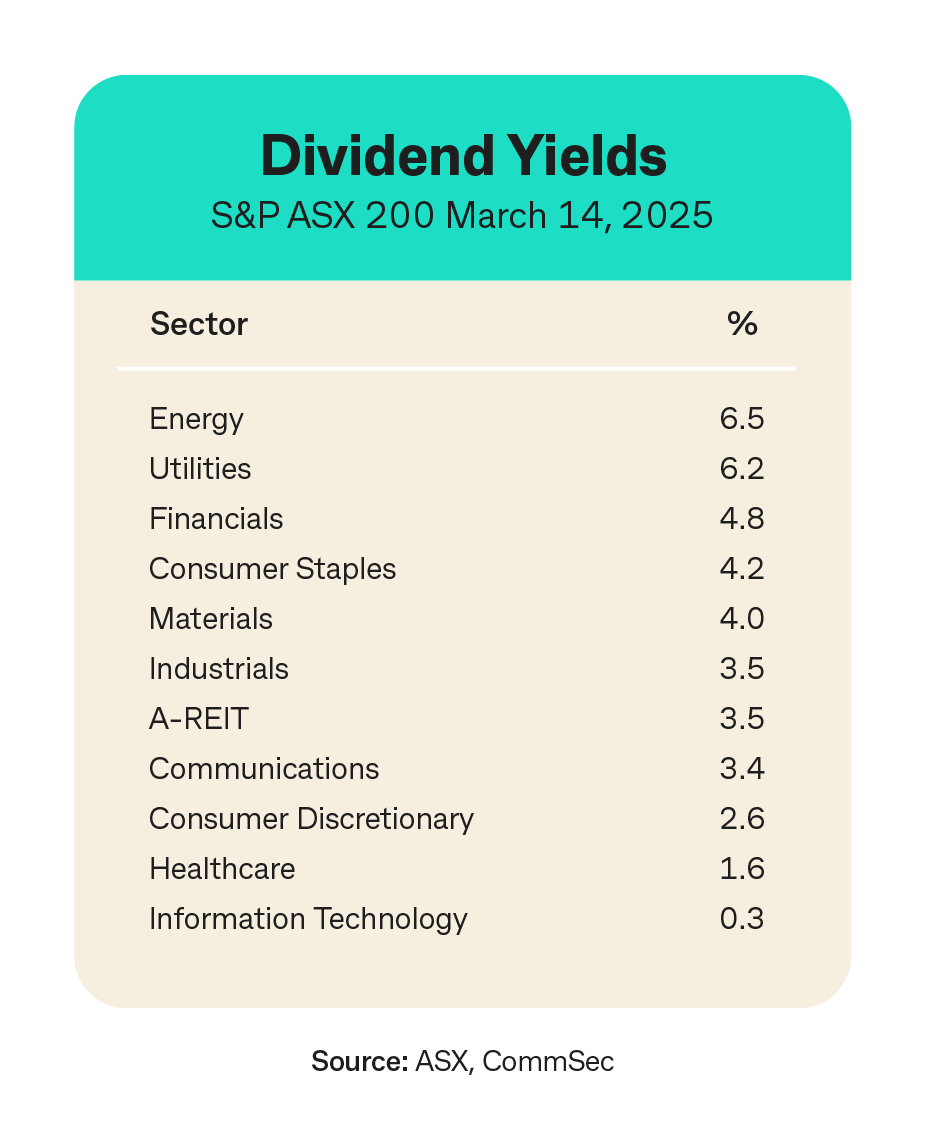

Despite the recent decline in dividend yields, several sectors of the Australian sharemarket still offer fairly attractive yields above the benchmark rate of 3.7 per cent. Energy shares have the highest trailing 12-month yield of 6.5 per cent, followed by utilities (6.2 per cent), financials (4.8 per cent), consumer staples (4.2 per cent) and materials (4.0 per cent), according to ASX data on March 14, 2025.

The data also shows that energy producer New Hope Corporation has the highest dividend yield at 10.5 per cent as of March 14, 2025. Poultry producer Inghams is next on 10.2 per cent, followed by Yancoal Australia (9.8 per cent), Fortescue (8.8 per cent), property services firm IPH Limited (8.4 per cent), Woodside Energy (8.2 per cent), toll roads operator Atlas Arteria (8.2 per cent) and investment manager, Magellan (8.2 per cent).

Another factor that makes dividends on shares attractive for many Australian investors is franking – or tax imputation – which gives them credit for the tax that has already been paid by the company in earning the dividend.

It is also worth pointing out that over the past five years, the total return of the S&P/ASX 200 High Dividend index, which includes the 50 highest-yielding companies in the ASX 200 with forecast positive yields, has climbed at an annualised rate of 9.5 per cent a year compared with 7.9 per cent for the S&P/ASX 200 index through to March 13, 2025.

In terms of the consensus outlook among local analysts, S&P/ASX 200 index aggregate market dividends are expected to ease around 5 per cent in Financial Year 2025, then grow by almost 5 per cent in Financial Year 2026.

Resources sector dividend growth is expected to fall a further 21 per cent in Financial Year 2025, contracting more sharply than the decline in earnings, partly due to lower payout ratios for the miners.

After several years of strong growth, banks sector dividend growth is expected to improve slightly with a 0.5 per cent increase in Financial Year 2025. Outside of the heavyweight resources and banks sector, dividend growth of around 4.5 per cent is expected for the year, though easing from a strong 8.5 per cent pace in the prior year.